One little-known junior explorer is grabbing attention for doing something that is virtually impossible: Landing a highly prospective and massive exploration concession that is almost always the purview of the major miners.

And the timing couldn't be better.

Panic over nuclear North Korea, a sudden military about-face in Syria, soaring Asian demand and recession talk is positioning gold for a major bull run, and Fiore Exploration (TSX:F.V; OTC:FIORF) has acquired one of the most attractive exploration packages in Chile—the hottest metals venue in the world.

The beginning of the gold turnaround came last year, but today--as global crisis hits fever pitch--we're looking at a bull run that will be bigger than anything we've seen in decades.

We are again at the point of urgency for getting in on gold, and there is no better venue than Latin America—the leading growth continent for the precious metal.

Fiore has scooped up almost all the best exploration territory surrounding the world-class El Penon gold mine owned by major player Yamana Gold. In a deal that a junior explorer could only manage if backed by heavy hitters, Fiore acquired a massive land package of three separate blocks.

Gold is being rendered even more attractive for Americans amid economic uncertainty most succinctly expressed by billionaire investor Warren Buffett of Berkshire Hathaway Inc., who noted that the U.S. is "less well equipped to handle a financial crisis today than we were in 2008." Central Banks the world over have also been stockpiling the precious metal since 2008, at levels not seen since before 1970.

One of the world's biggest legends in mining, Canadian billionaire Frank Giustra, who is also the founder of Lionsgate Entertainment Corporation, is pouncing on gold voraciously, and where his gold money goes, markets tend to follow. He's also the heavy hitter backing Fiore.

The big money to be made in gold is in exploration, especially if you can find a junior backed by legendary mining money and a dream team of explorers. Giustra's hitched his wagon to several already—but only those with dream teams and exceptional vision. He hasn't been wrong yet.

Here are 5 reasons to keep a very close eye on Fiore Exploration (TSX:F.V; OTC:FIORF):

#1 Billion-Dollar Deal-Closing Team Backed by Heavy Hitters

The team behind Fiore has been in Chile—the No. 1 mining venue in South America—for over 20 years.

CEO Tim Warman is a 25-year mining veteran perhaps best known for helping to close a $1.2-billion deal with Kinross. Warman has a long track record of making multi-million-dollar discoveries and keeping his shareholders very happy, both with Aurelian Resources and Dalradian. In fact, Aurelian sold to Kinross for $1.2 billion, while Dalradian's stock hit a market cap of a couple hundred million dollars.

He's also well-known at Barrick Gold, whose 6.8-million-ounce Alturas deposit was discovered by Malbex—a company Warman used to run.

Besides Warman, one of the most sought-after geologists on the mining scene, the team also includes Brian Paes-Braga and Paul Matysek, two more heavy weights with impressive track records.

Paes-Braga is best known as the founder and CEO of one of the most striking junior lithium companies to hit the scene since the electric vehicle (EV) boom sparked the lithium craze. And Matysek has created shareholder value of well over $2 billion in gold, lithium, potash and uranium.

With this dream team behind it, Fiore is anything but your average drill play.

#2 Early In, Pinging Investor Radar

Fiore has grabbed attention in a space where only the majors get it, because it's managed to secure the permits to surround Yamana's majestic El Peñon Gold mine. Yamana produced 227,000 ounces of gold and 7.7 million ounces of silver last year alone—worth $286 million and $130 million, respectively.

Fiore's (TSX:F.V; OTC:FIORF) entrance onto this scene was explosive, and a headline-grabbing surprise.

These are first-movers parked right next to a major producing gold mine, and they're ready to take on more—Pampas is just a starter project, but a big one backed by heavy hitters.

And it doesn't stop here, the company is currently looking into the acquisition of equally prospective properties. A development we expect to hear about any day.

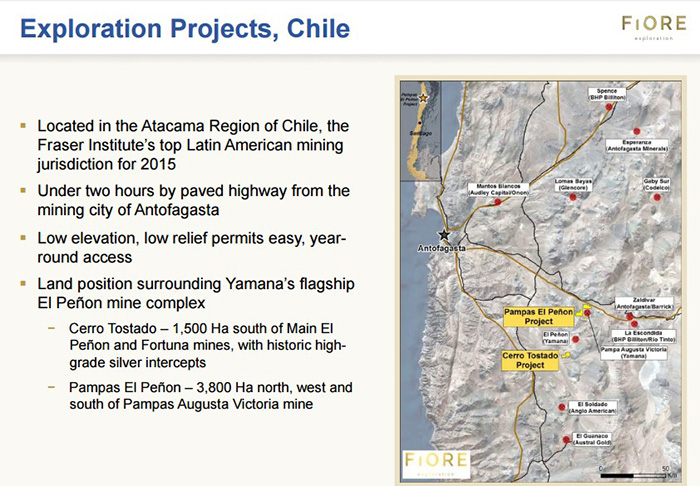

#3 Next Door to a Huge Mine

In the industry, 'closeology' is one of the deciding factor of success—and Fiore has it in droves.

Yamana's El Peñón mine is one of the most prolific gold and silver mines in Latin America, whether we're talking about either size or grade. It's massive, and its high-grade.

El Peñón has produced over 3 million ounces of world-class gold and more than 90 million ounces of silver since it went into production in 2000. Annually, this mine accounts for 18 percent of Yamana's gold production, and annually it produces nearly 230,000 ounces of gold for the company. And there's still a lot to come: We're still looking at 2.4 million ounces of gold left in the mine, and another 77 million ounces of silver.

Fiore now surrounds this massive mine on three sides, so they've inherited all the infrastructure, and a massive exploration patch in a known money-maker. In fact, you can stand on Fiore's land and throw a rock into Yamana's pit.

And Fiore's leadership has great relationships with the corporate teams of the majors it's right next to, so they have access to the grounds that the average junior minor wouldn't. It's not just Yamana, it's also Chilean giant SQM—a relationship that goes a long way toward getting things done in Chile.

Now Fiore's got a second major project, Cerro Tostado—again, flanking Yamana and just north or Anglo American's El Soldado mine and Austral Gold's El Guanaco mine.

And it gets bigger, still. In April, Fiore acquired the Rio Loa gold exploration project in Chile's prolific Maricunga belt. This—again—is right next to another major mine, the Gold Field's 3.3-million-ounce Salares Norte discovery. Salares Norte is one of the highest-grade gold deposits in this belt, which boasts more than 100 million ounces of gold in reserves, resources and past production.

Fiore is hungry for undervalued assets in known mining districts with multi-million-ounce deposits, and investors are going to love it.

#4 Well-Financed (Follow the Legendary Mining Money)

Fiore (TSX:F.V; OTC:FIORF) breaks the mold when it comes to small-cap gold miners in more ways than one. There's nothing an investor likes more than a company with positive cash flow and the ability to raise capital with the snap of the fingers.

Fiore is backed by legendary financer Frank Giustra, so with big money following its dream team around, Fiore has no trouble raising the capital it needs to drill. This gives Fiore access to capital that most juniors don't have, and last year alone they raised $16 million.

Giustra, the Canadian business mogul who really needs no introduction as he has financed countless high-level natural resource deals, is known for financing the right mining deals at just the right time. So much so that it has become known in industry circles as the "Giustra Premium", which is exactly why Fiore is so well followed at this stage.

Fiore is already heavily funded—more than enough for its current exploration program, and more acquisitions are in the future.

#5 Drilling Results Soon

Fiore completed drilling an 8,000-meter RC drill program in December. The first drilling results at Pampas El Peñon have been promising, and follow-up drilling is planned before mid-year. Over $1 million has already been spent and most of the mapping, sampling, trenching and near-surface drilling has been completed—all showing similarities to the major gold reserves right next to it.

Three areas within rhyolitic domes with breccias and favorable geochemistry were identified and as priority drill targets—all of them in immediate vicinity of the Pampa Augusta Victoria open-pit and underground mines.

And this week already Fiore will kick off its drilling program at Cerro Tostado, with initial results coming in subsequent weeks.

And the previous work done here by Chile's SQM was already promising. The results of some 1,937 meters of reverse-circulation drilling in 17 holes confirmed the presence of structurally controlled silver-dominated mineralization, with highly anomalous levels of silver, arsenic and antimony and anomalous levels of lead and zinc.

To Re-Cap:

With Fiore, we've got a unique junior explorer here that has done something that juniors just don't do: Flanked major miners in a flurry of acquisitions that we already know are highly prospective for gold and silver. Even better—they've got heavy weight backing to take this to the finish line. And with drilling results set to come in soon, this finish line is getting close, fast.

And the time is now—for gold.

Giustra is putting his money where his mouth is—and so far he's been spot on. He recently told an audience at a Vancouver investment conference that the worsening political and economic uncertainty on the global stage was going to feed an incredibly bullish gold market--one that could quite possibly surpass the $1900 an ounce mark. So, says Giustra, if you're looking at gold as an investor, you've got to get in now because this window is closing fast. That's why he has major money in three gold explorers right now.

This is a rare chance to get in on a cycle opportunity for unexplored, under-explored and undervalued precious metals in Latin America, and the whole set-up with Fiore (TSX:F.V; OTC:FIORF) potentially offers more reward than risk.

Here are some more big Canadian listedplayers worth watching:

IAMGOLD Corporation (TSX:IAG) (NYSE:IAG): IAMGOLD has been getting a fair amount of attention lately because while it's shares have dipped since they hit their peak in the summer of 2016—and they are still weak—but they are gaining now, so it might be a good time to get in while undervalued.

Cameco Corporation (TSX:CCO) (NYSE:CCJ): Cameco—a US$4.52-billion market cap company--is trading at a major discount to its intrinsic value right now, and it's a good play for dividend-focused investors.

OceanaGold Corporation (TSX:OCG): OCG's shares have been relatively flat over the past year, but there are some production catalysts that could make this good timing. Headquartered in Australia, OCG has gold and copper assets in the Philippines, New Zealand and the US, and is expected to produce up to 170,000 ounces of gold this year—at attractively low production costs.

NewGold Inc. (TSX:NGD): NewGold's Q1 operational results were pretty impressive, particularly with respect to considerably lower all-in sustaining costs (down $160 per ounce compared to the same time last year).

Hecla Mining (NYSE:HL): 2016 was a big year for Hecla (market cap US$2.04 billion), with silver production up 48% and gold up 24%, though 2017's production targets won't be as big.

Agnico Eagle Mines (NYSE:AEM): Any more upside in this miner and it will go directly to shareholders. This has been one of the best performers in recent years, and most attribute it to great asset management and fiscal conservatism that has resulted in low-cost production.

Legal Disclaimer/Disclosure: This piece is an advertorial and has been paid for. This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment. No information in this Report should be construed as individualized investment advice. A licensed financial advisor should be consulted prior to making any investment decision. We make no guarantee, representation or warranty and accept no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of Baystreet.ca only and are subject to change without notice. Baystreet.ca assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission. Furthermore, we assume no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information, provided within this Report.