There are those in the industry that choose to follow the status quo and continue operating as though the current modus operandi will go on forever. But on the new horizon of the energy revolution, there are companies like Tesla Motors and Pure Energy Minerals (TSX.V:PE / OTC:PEMIF), who understand that the status quo isn’t good enough.

While Tesla has set the standard for electric vehicles and has forged ahead with the largest lithium ion battery factory in the world, Pure Energy is forging ahead with a new production method for lithium—the hottest commodity on the market right now, and the one that forms the backbone of the energy revolution.

Combining the Best Attributes of Hard Rock and Brine Operations

In the lithium world, there are two primary natural sources from which lithium is extracted: spodumene and brine. While lithium brine operations tend to be lower cost, they suffer from a lot of inefficiencies and take years to ramp up. The sun’s evaporation is a huge bottleneck in production schedules, while hard rock deposits are only limited by mine construction schedules.

Recently, Pure Energy and its partner in development, Tenova Bateman Technologies (TBT), achieved a breakthrough in the successful testing of their unique method of lithium brine processing. The three-step process - which includes pre-treatment, solvent extraction, and electrolysis – goes from mineral in the ground to final lithium hydroxide without the need for evaporation ponds. More to the point, the new process could allow Pure Energy to launch operations just as fast as hard rock miners, while producing at costs comparable to brine operations.

It’s an evolutionary breakthrough for a revolutionary mineral.

Ahead of the Nevada Junior Crowd

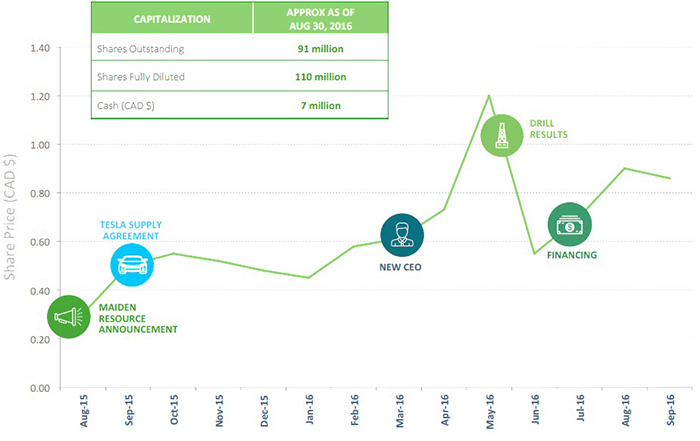

Many of the lithium juniors in the continental U.S. are just getting their feet wet, getting funding to determine scope and magnitude of resource estimates, while already Pure Energy has obtained results from its Phase 3 drilling program.

The company has started to move to the economic study portion of its development, with its Preliminary Economic Assessment (PEA) due in the next few months. While most companies are looking to delineate their resources and understand what, if anything, they are actually sitting on, Pure Energy is looking further down the road, already eyeing a reduction in start-up time through its unique extraction process.

With the PEA planned to be issued soon, Pure Energy is well on its way to becoming the first junior in the U.S. to move from mineral resources to reserves. Having already engaged in the permitting process, it’s also on track to be the first to obtain a permit to build a mine.

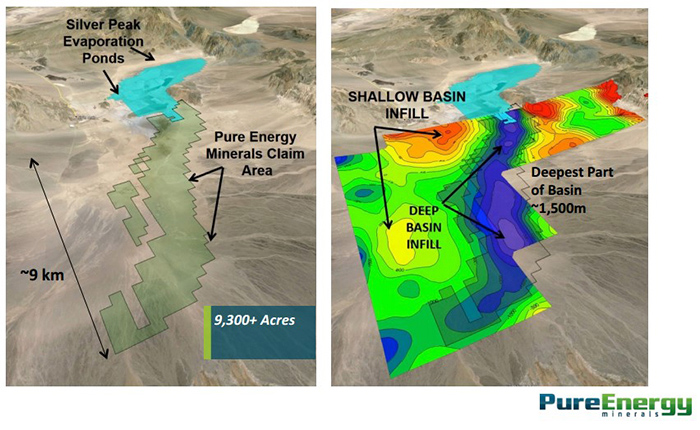

So not only is Pure Energy sitting on more than 11,000 acres in the heart of the lithium land rush at Clayton Valley, Nevada—adjacent to North America’s only producing lithium mine—but it’s also way ahead of the game here and it’s likely to be the first out of the gate for new production.

It’s not coincidental, either. This is a company with zero debt, a strong balance sheet and a dream team of individuals with an impressive combination of experience in discovery, hydrogeology, lithium processing, project development, fundraising, as well as mergers and acquisitions.

Pure Energy’s Clayton Valley South Project has an inferred mineral resource of 816,000 tonnes of lithium carbonate equivalent, and its processing breakthrough gives it an edge in the race to become the next major supplier in a market that is panicked over new supply.

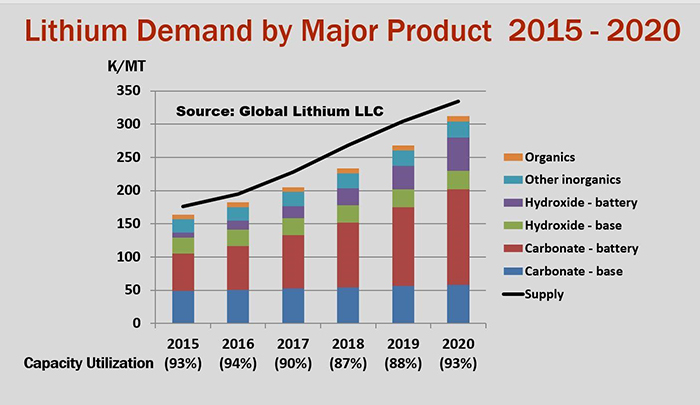

Demand-Side Estimates Continually Revised Upwards

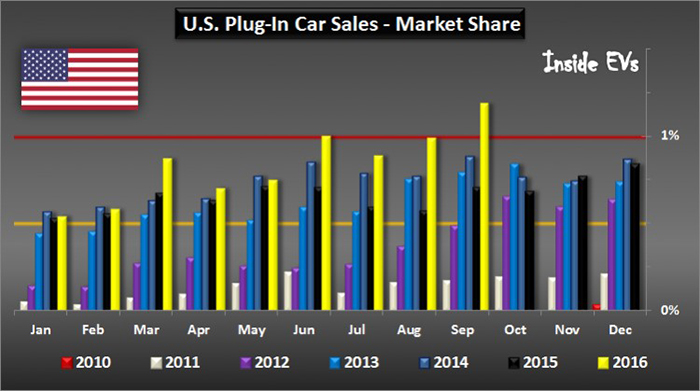

September marked the first month in history that U.S. electric car (“EVs”) sales were over 1% of total sales, coming in at 1.15%, with total year-to-date sales of over 108,000, over 115,000 North America wide. The North American Market is expected to reach 175,000 by the end of the year. Everyone’s getting on board, including Audi (ETR:NSU), BMW (ETR:BMW), Mercedes (DAI:XE), Lexus (NYSE:TM) and Volkswagen (ETR:VOW3). One of the biggest players in the world—General Motors (NYSE:GM)—is planning to mass produce the Chevy Bolt EV by 2017-2018, eyeing 30,000 cars already next year.

Europe sold 125,000 EV’s as of August, with annual sales expected to come in at 200,000. China has sold 193,000 units as of August, with some predicting 450,000 units by year end. Combined with other markets like Japan and Australia, the projection tops 900,000 units for the world in 2016. That would mean another year of +60 percent year-over-year growth in EV sales.

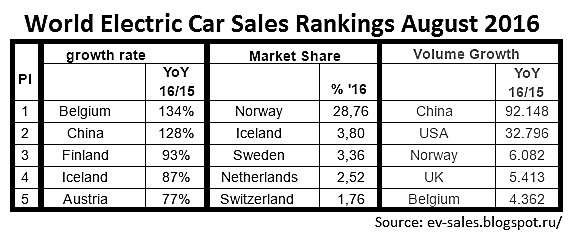

These are exciting projections, but the record increase in September numbers for the U.S. are even more striking when combined with the record volume growth in some European markets like Belgium, Austria, and Germany – where a new incentive program saw the country break the 1% mark for the first time in September. 2016 will mark over 1% electric vehicle penetration globally, and if the current rates hold, that means 5 million EV’s or 6% global market share by 2020.

Assuming an average 30 kWh battery pack across the spectrum of electric cars and 0.814 kg per kWh, that means that 2016 EV sales alone will require almost 22,000 tonnes of lithium carbonate equivalent. Considering the huge increase from 550,000 EV’s in 2015, it looks like another 8,500 tonnes of the metal will be required just for new electric car sales this year. With a new lithium mine coming in at around 15,000 tonnes of lithium carbonate each year, the lithium demand from just the increase in EV sales this year will account for more than half of one good-sized new mine.

By 2020, projected new EV sales will consume over 122,000 tonnes a year – or five to eight lithium mines.

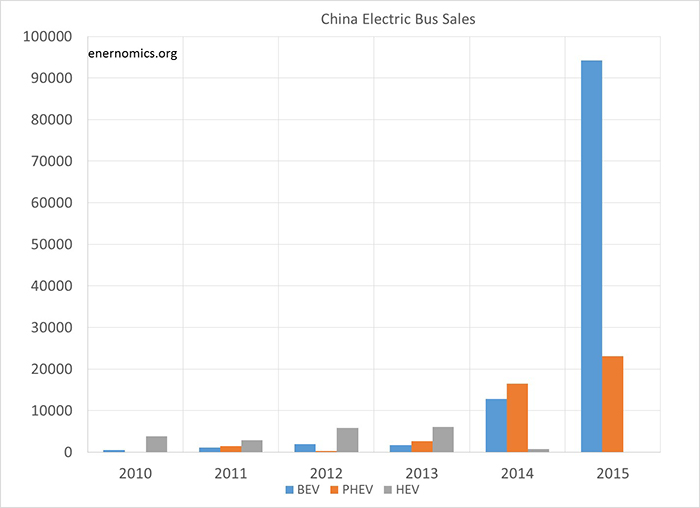

Electric Bus Sales Exploding

Although the true numbers could come in lower considering the fraud that has recently come to light iin the Chinese electric bus industry, the numbers are still staggering. Even if there were only half the BEVs sold in 2016, each bus requires up to 10 times as much lithium. This translates into 50,000 buses requiring almost 8,000 tonnes of lithium carbonate – and this is only the Battery Electric Buses in one country.

This untapped market by itself could put the world’s lithium supply on its knees.

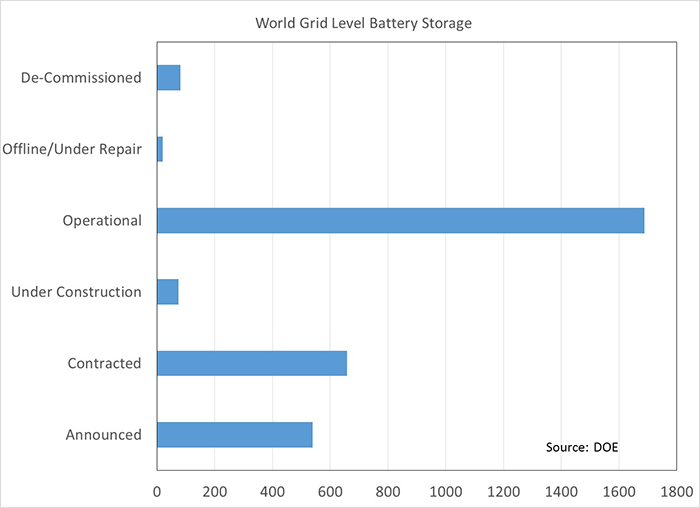

Grid Storage: The Battery Market’s Underdog

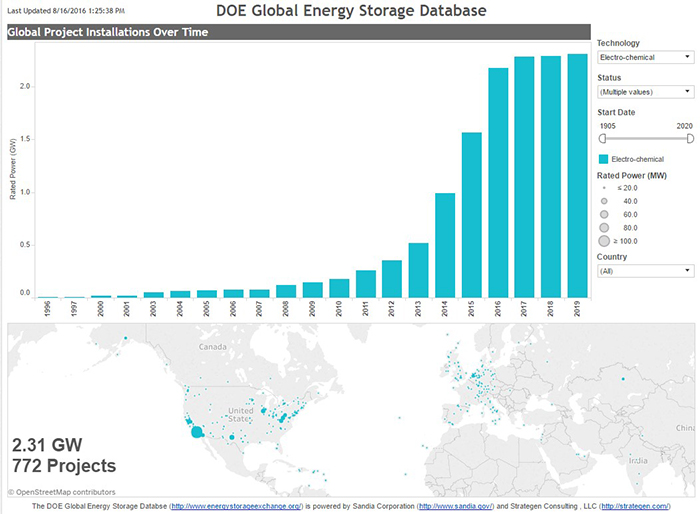

The largest potential market for Lithium, however, is grid storage—and this is a wildcard that is just getting started. To date, the U.S. Department of Energy has listed almost 750 grid-level storage projects coming in at around 2,400 tonnes of lithium carbonate.

Until now, most electric storage favored pumped storage, with the pumped storage capacity coming in at 60 times the grid-level battery storage. However, the pump-turbine efficiency lowers potential output by around 70% of input, while batteries can operate closer to 98%. As the price of water goes up and fewer favorable geographies can be found, batteries will come into favor over pumped storage. This suggests a huge potential increase for grid storage batteries, without considering the effects of increased wind and solar power.

Quoting one of the most respected names in the lithium sphere, Joe Lowry:

“We are in the beginning of a long term cycle of significant lithium demand growth and are ending a cycle of significant underinvestment in lithium supply. No matter what certain “experts” say – supply and demand are NOT in balance. If the market is adequately supplied, why are we having the current price run-up?”

Simply put, lithium supply is not coming online fast enough to keep up with demand. New supply from places like Argentina, where lithium is extracted using older technology, will not come online until at least 2020. This leaves hard rock operations and innovators like Pure Energy to pick up the slack.

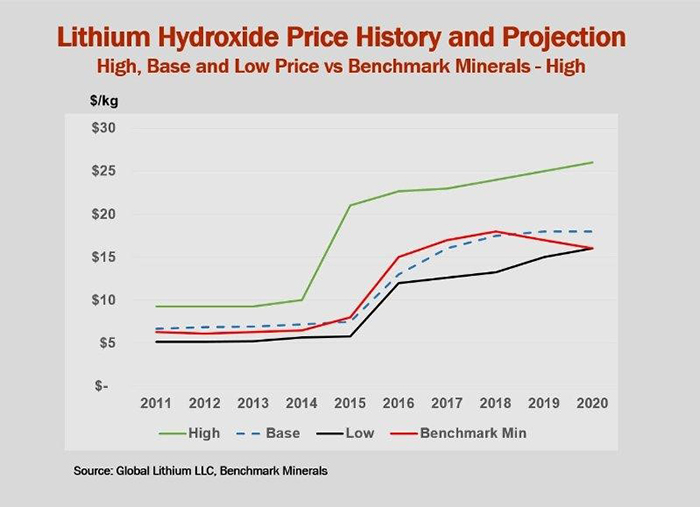

Another key difference is that a premium will be paid for those able to produce lithium hydroxide (LiOH) over lithium carbonate (Li2CO3).

More and more high-end battery manufacturers prefer lithium hydroxide, which can require additional processing of carbonate prior to use in batteries. This is part of the reason for the premium paid for hydroxide over carbonate – and Pure Energy has designed a process to produce hydroxide directly.

Estimates show that five new lithium mines will be needed by 2020 using conservative numbers, with eight using more aggressive growth numbers.

Investors have been watching the new lithium entrants with increasing interest over the past year. Smart investors are waiting to see who will emerge at the front of the pack to take advantage of the voracious demand that could lead to this lucrative supply gap. The leader has emerged as Pure Energy—the North American company that has come the farthest, and is in the right place at the right time.

Investors have been watching the new lithium entrants with increasing interest over the past year. Smart investors are waiting to see who will emerge at the front of the pack to take advantage of the voracious demand that could lead to this lucrative supply gap. The leader has emerged as Pure Energy—the North American company that has come the farthest, and is in the right place at the right time.

In today’s market there are those who stick with the tried and true method for too long - only to see their fortunes turn negatively, and those who strive to change the game - to improve. The world belongs to the pioneers, and Pure Energy is proving itself to be a true lithium pioneer in the US.

Legal Disclaimer/Disclosure: This piece is an advertorial and has been paid for. This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment. No information in this Report should be construed as individualized investment advice. A licensed financial advisor should be consulted prior to making any investment decision. We make no guarantee, representation or warranty and accept no responsibility or liability as to its accuracy or completeness. Expressions of opinion are subject to change without notice. We assume no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission. Furthermore, we assume no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information, provided within this Report.