As China moves stealthily on the world’s cobalt and lithium supplies to feed an unprecedented US$360-billion renewable energy push, watch what happens next in Chile, where Chinese investors are talking about a mega $2-billion battery factory to rival Tesla.

Tesla in January switched on the power at its Nevada battery gigafactory—and we’re just getting started here. Battery factories are popping up all over Europe as well.

SGF Energy is planning a gigafactory in Sweden. Later this year, two are expected to open: BMC’s in Germany and LG Chem’s in Poland. Samsung is also eyeing a gigafactory in Hungary next year.

And while the supply of batteries is about to sky-rocket, the lithium that feeds them will ultimately depend on new supply by emerging small-cap explorers like LiCo Energy Metals (TSX:LIC.V; OTCQB:WCTXF).

But there’s a twist to this small-cap that should start making an investor’s radar ping: While everyone’s caught on to the lucrative lithium story, cobalt—another major lynchpin of the gigfactory equation—is overlooked. And LiCo—as its names suggests—is after market share in both.

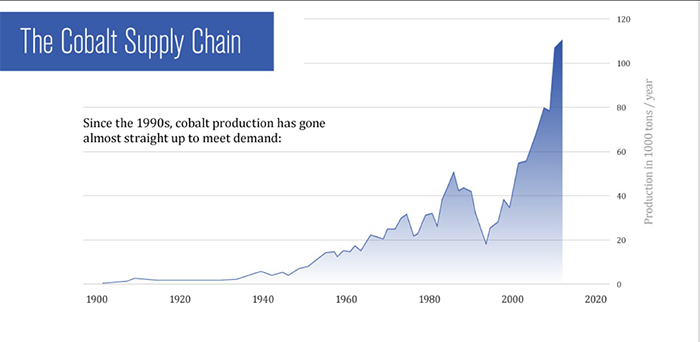

Cobalt supply is even more elusive than lithium supply, and the industry currently uses 42 percent of global cobalt production with the remaining 58 percent going to diverse industrial and military applications.

Companies like Tesla (NASDAQ:TSLA) and Panasonic (NYSE:PC) need reliable sources of the metal, and the supply chain is anything but, because 97 percent of it is just an afterthought—mined and brought to market as a by-product of nickel or copper. And as the price of nickel and copper continue to plunge, it makes mining them uneconomical, further tightening the cobalt supply picture. And even worse, some 60 percent of it comes from the unstable—and questionably sourced—Democratic Republic of Congo (DRC).

Source: Visual Capitalist

The auto industry doesn’t like to source its cobalt from here because any connections to this supply chain are bad for reputation in terms of corporate social responsibility. China, however, has no such qualms.

Where does that leave us? Canada: It’s the only major venue left under control for new supply, and it’s already the #3 cobalt producer in the world. And LiCo is mining pure cobalt here—not as a by-product of nickel or copper.

Sitting on the Highest Grade of Lithium in the World

The fact that Chinese and Korean investors are in advanced talks for a US$2-billion mega-lithium battery plant in Chile is no coincidence. Chile has vast salt flats that hold enough lithium to supply the world for decades—and this exactly where LiCo has positioned itself.

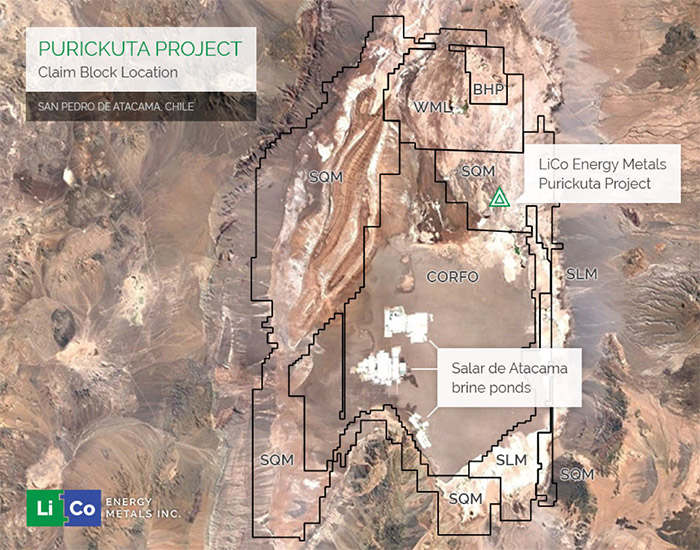

LiCo (TSX:LIC.V; OTCQB:WCTXF) is one of the fastest-moving new small-cap explorers on this tight supply scene, and it has just acquired interest in a major exploration project in Chile’s prized lithium development, Salar de Atacama, home to around 37 percent of the world’s entire lithium production.

LiCo—which will take on up to a 60 percent interest in the Purickuta Project—is now exposed to one of the best new lithium supplies in the world. The project covers 160 hectares and is one of a few exploitation concessions granted within the highly sought-after Salar de Atacama.

It is surrounded by major lithium mining and is right in the middle of an existing exploitation concession owned by mining major Sociedad Quimica y Minera (NYSE: SQM) and only 3 kilometers north of another exploitation concession of CORFO (the Chilean Economic Development Agency). Some 22 kilometers south-east of this project, SQM and Albemarle have large-scale production facilities, two of which produce, combined, over 62,000 tonnes of Lithium Carbonate Equivalent annually. They account for 100 percent of Chile’s existing lithium output.

Even better: Salar de Atacama’s lithium is easier and cheaper to produce than anywhere else in the world because its high-grade lithium and potassium has a high rate of evaporation and extremely low annual rainfall.

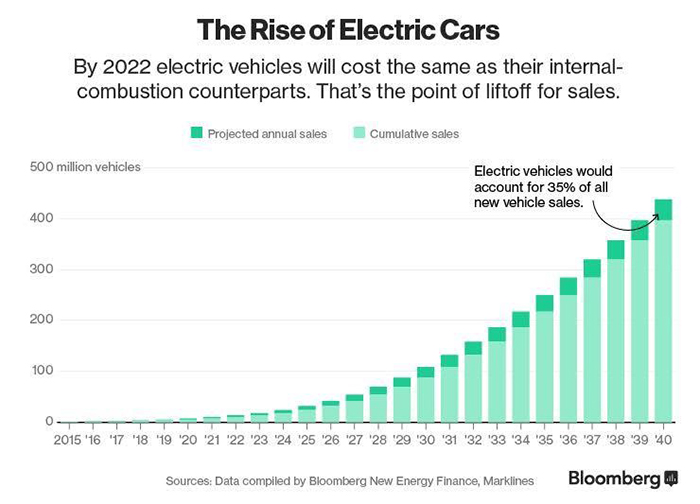

There’s no better place to be when you consider that demand for lithium is projected—at the least—to more than double over the next 8-9 years, according to Deutsche Bank. But that projection doesn’t scratch the surface of what’s to come as the electric vehicle boom accelerates. Tesla may be in the lead right now, but the competition is becoming fierce. Everyone’s trying to cut in on this, from BMW and Volkswagen to Daimler’s Mercedes Benz. And Tesla’s momentum alone is enough to make lithium demand phenomenal: By next year already, Tesla is predicting that it will double global battery production capacity.

EVs aren’t only gaining traction in the global mainstream—they’re set to overtake traditional vehicles sooner rather than later. By 2022, according to Bloomberg, EVs will be cheaper than traditional vehicles.

So it’s a great time to be sitting on top of the world’s best lithium supplies.

Cobalt: If it’s Not ‘Pure’, It’s Not Enough

By 2020, it is estimated that one-fifth of cobalt demand will come from EVs. DRC is out—no reputable company wants to source its cobalt from here. That leaves North America, which currently produces only about 4 percent of global supply. That’s not enough for even 500,000 of Tesla’s new Model 3 EVs, which need about 6 percent of the world’s supply.

This is where LiCo finds itself in an entirely unique position. The cobalt supply that does exist is ‘accidental’ for the most part, and dependent on the price of nickel and copper. If prices don’t make sense for nickel and copper, no cobalt is mined, since it is simply a by-product. None of the global supply comes from pure cobalt plays. LiCo’s project is pure cobalt.

The company’s Teledyne Cobalt Project is a high-grade, advanced-stage cobalt project in the heart of a historical mining district in Ontario, Canada. Covering 11 claims across over 1,368 acres, this project already boasts CAD$25 million in inflation-adjusted infrastructure.

LiCo has hit the ground running with its CAD$700,000 exploration program on its cobalt property, and we expect big things very soon.

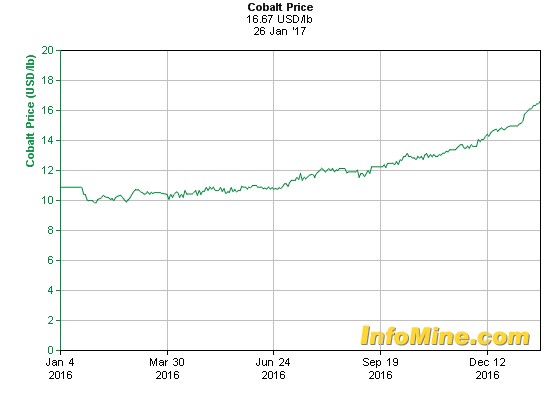

Cobalt prices are already soaring: In the last six months, they’re up 70 percent.

And that 70 percent price spike may soon seem meager, with CRU estimating a 12,000-tonne deficit—at least—by 2020.

New supply for the metals feeding our resounding energy revolution are going to come, in large part, from small-cap companies who are staking new claims and breaking the status quo. If you can find a strong small-cap lithium explorer with savvy management and a solid balance sheet—that’s great. But when you find one that’s targeting both lithium and cobalt—the upside is twice as good.

When you have two high-demand metals, low-cost resource definitions and near-term production in the top two venues in the world—you have a powerful scenario.

Legal Disclaimer/Disclosure: This piece is an advertorial and has been paid for. This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment. No information in this Report should be construed as individualized investment advice. A licensed financial advisor should be consulted prior to making any investment decision. We make no guarantee, representation or warranty and accept no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of Baystreet.ca only and are subject to change without notice. Baystreet.ca assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission. Furthermore, we assume no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information, provided within this Report