One little-known company is seeking to position itself at the forefront of the Fourth Industrial Revolution.

It is seeking to take advantage of a potentially multi-billion-dollar oversight by companies like Google, Facebook, Apple and Amazon.

Some of the most powerful companies on Earth could be facing an existential threat…from a company that you’ve likely never heard of.

Frankly Inc. (TSXV:TLK, OTCQX:FRNKF) is a tiny firm with huge plans for the future.

It has tapped into the three most valuable sectors in the tech space: engagement, monetization and data collection. And it hopes to teach the Big Tech cartel a very painful lesson.

Big Tech has proven to be both greedy and overbearing, driving publishers to look for new and more flexible partners. This trend saw Facebook and Google lose advertising market share for the first time ever last year.

And now Frankly is looking to deliver another blow to these bloated and dated industry giants.

Frankly has already built up a user base of 100 million, and at an average user value of $175 each, that’s an asset worth $17.5 billion.

Even if it seizes just 1% of the digital ad market, Frankly could see its revenue stream top $1 billion.

And that’s just the beginning.

The tide could be turning away from Big Tech, and this little $30 million firm appears ready to bust the market wide open.

#1 A Better Way To Publish

Big Tech is falling out of favor with some of its biggest customers…

Companies like Google and Facebook have become greedy and overstayed their welcome…

And publishers have had enough.

That’s where Frankly (TSXV:TLK, OTCQX:FRNKF) comes in…

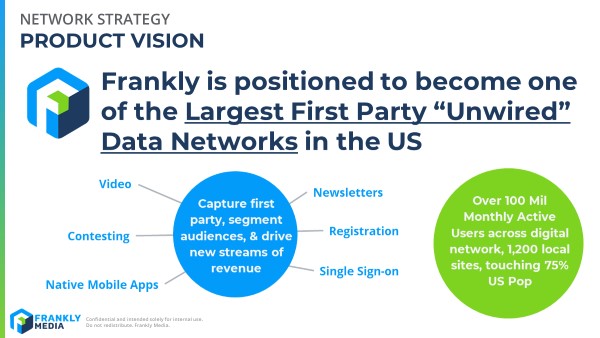

Frankly is a new platform for publishers who can’t catch a break with Big Tech.

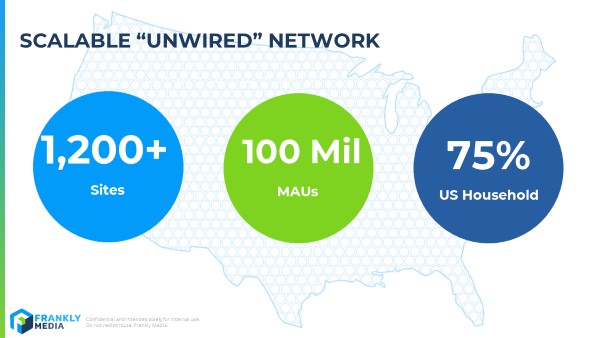

It already has close to 100 million monthly active users (MAUs), with 1,200 digital news, information, and entertainment properties across the United States. On this scale, Frankly can reach 75% of American households.

And it could be about to get bigger.

Frankly is capturing market share from Google and Facebook. The company has just announced a $50 million partnership with Newsweek, adding 40 million MAUs and offering the company a way to capture first party data through a host of different touch points.

An even bigger announcement came in July—Frankly acquired Vemba, a leading video asset management, syndication and monetarization platform.

What Vemba does—and what Frankly can now harness for its own needs—is monetize video streaming by providing syndicated video-on-demand.

Through Vemba, Frankly can manage, track and monetize video delivered across its network of over 1200 sites and access hundreds of different media outlets—including CNN and its 1,100 affiliates and Vice Media.

Over-The-Top (OTT) Video market is expected to reach $332 billion by 2025, according to Allied Market Research.

Google and Facebook are already losing advertising market share.

Frankly’s acquisitions, partnerships, and in-roads into things like OTT Video position it to become a real competitor for ad dollars.

And remember—even 1% of this $100 billion market could turn Frankly (TSXV:TLK, OTCQX:FRNKF) into a billion-dollar firm.

#2 Frankly’s Biggest Strength

Frankly’s business is a little technical. But here’s how it breaks down:

The company takes content from publishers—TV broadcasters, radio broadcasters, and faith-based organizations—and broadens exposure across thousands of points of contact.

Frankly can then harness first party data to deliver content specifically tailored to users’ profile.

And using this data means that Frankly can target key demographics—particularly conservative, Christian Americans left behind by the Big Tech’s media bias.

Frankly Faith, for instance, works at delivering content from publishers working to grow their gatherings.

And the reviews are in:

“The Frankly Faith team is great to work with…We are thrilled with our partnership…They’ve really helped us get noticed.”

Frankly (TSXV:TLK, OTCQX:FRNKF) understands the media climate in 2019, and knows that demand out there for a reliable alternative to Big Tech is huge and growing.

With more than 1,100 outlets and hundreds of partnerships, Frankly can handle 1-2 billion ads per month, delivered to 100 million MAUs.

Heading into the 2020 election, the demand for reliable content and coverage will be greater than ever.

#3 The Multi-Billion Dollar Mistake

Speaking of elections…

It’s become pretty clear that Big Tech has a problem: liberal bias.

Google and Facebook censor conservative news and opinion. Members of the public feel that Big Tech are unfair to conservative Americans.

Social media has been “weaponized,” according to political strategist Ed Goeas, and President Trump himself believes Facebook and Google have “taken advantage of people” by manipulating search results.

Twitter has been called the worst offender—conservative thought-leaders have been kicked off the platform, and according to Richard Walters of the Republican National Committee the company has shown a “disgusting bias” in how it’s treated conservative figures.

“Facebook refuses to publicly acknowledge that conservatives have been disproportionately affected by their content policies,” said Brent Bozell, head of the Media Research Center.

The liberal bias among Big Tech shouldn’t be that surprising—the companies are based in San Francisco and backed Hilary Clinton in the 2016 election—but the real news is what this mistake will cost the tech companies on the digital ad market.

Advertisers for respectable, family-friendly companies—Wal-Mart, Hobby Lobby, Chick Fil A—have all expressed concern about this bias.

And Big Tech is now under more scrutiny than ever—Congressional hearings are just the tip of the iceberg.

There seems to be a groundswell against the dominance of Big Tech.

And Frankly (TSXV:TLK, OTCQX:FRNKF) is looking to cash in.

#4 The Data Difference

Frankly is not only setting itself apart as an unbiased alternative to Big Tech’s liberal-leaning dominance…

It’s also giving publishers more freedom to take control over their advertisements.

Every ad you see online aims at one thing: your attention.

It’s what advertising is all about. Capturing your interest and linking it to a good or service.

The golden ticket is first party data—information linking directly to a user. This can include personal data, past purchases and product interests.

Let’s say you’re a gear-head who spends a chunk of time online browsing the latest tech. That data is a gold mine for advertisers, who can target content directly to you, the first party user.

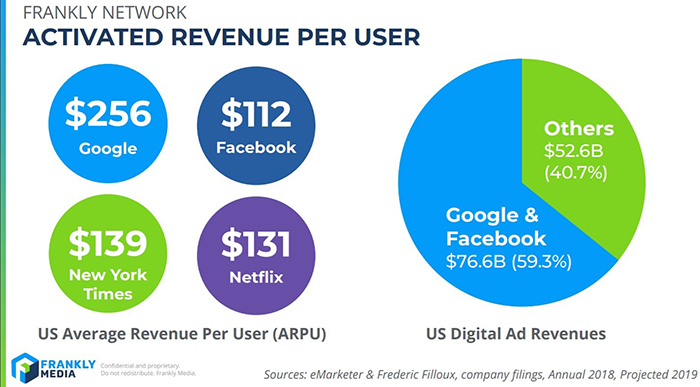

Activated revenue per user (ARPU) measures how much is captured through first party data. For the biggest internet firms, this is where the real money is—Facebook and Google between them net $76.6 billion in ad sales, realizing $112 and $256 ARPU, respectively.

In the last seven years, the market around capturing first party data through digital ad sales has exploded.

Digital ad spending has increased by 350% from $32 billion to $111 billion.

By one estimate, digital advertising could reach $665 billion by 2026.

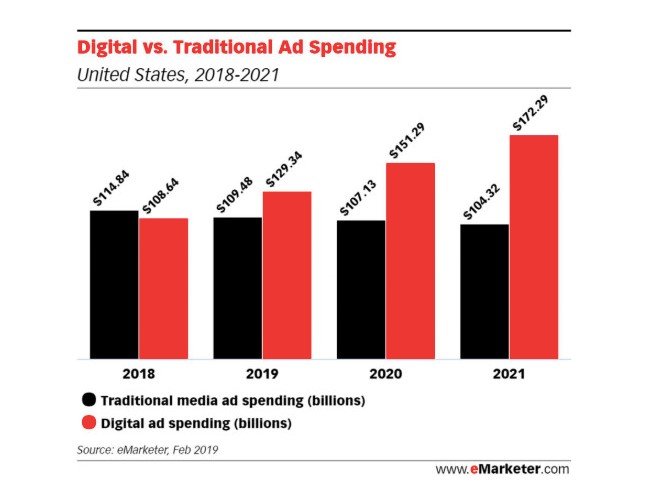

Advertisers now spend far more on digital ads then on traditional print media- $129 billion compared to $109 billion, according to eMarketer.

And Google and Facebook make up 60% of that digital ad market, bringing in a combined $77 billion.

Compare that to the New York Times, which earns a mere $259 million from digital ad sales.

Other industry giants, like Newsweek, are struggling with the same problem – market dominance from Google and Facebook.

Apple is also attempting to get in on this game, creating a digital news service—“Netflix for News”—with subscriber revenue split between Apple and publisher partners. But even in this system, publishers will be forced to accept giving up a larger and larger chunk of their revenue as the platform grows.

That’s pretty typical. In general, Big Tech doesn’t share much with the publishers, hoarding the user value for themselves. Publishers are just hanging on, desperately searching for ways around the big firms.

The competition is real. And Frankly only needs a sliver of this massive, growing market—say 1 percent—to realize huge earnings: just that small portion would yield Frankly more than $1 billion in revenue.

With 100 million monthly active users (MAUs), each potentially worth $175, Frankly may have already secured a $17.5 billion asset.

And that’s before you consider what makes Frankly (TSXV:TLK, OTCQX:FRNKF) different from all the rest…and where it has an edge on Big Tech.

#5 The Timing Could Not Be Better

Frankly is a tiny company: worth just $40 million.

But it’s growing fast.

The new deal with Newsweek has increased its user base by nearly 50%.

This tiny $40 million market cap company is already sitting on an asset that’s potentially worth $17.5 billion, working on breaking into a market worth $100 billion…a global market that could be worth $600 billion in less than a decade.

And now Big Tech is in decline. Users are turned off and publishers are looking for alternatives.. the timing could not be better for this game-changing company.

Frankly can already reach 75% of all Americans and its deals with Vemba and Newsweek will expand that reach even further.

If you missed out on Facebook’s astounding 800% boom to a $500 billion market cap, or Google’s 670% growth to an $800 billion market cap – then this may be your chance for redemption.

A new platform harnessing first party data to deliver cutting-edge results to advertisers, all in a way that doesn’t alienate ordinary American consumers.

The next phase of the Fourth Industrial Revolution is already underway, and Frankly (TSXV:TLK, OTCQX:FRNKF) is hoping to lead the charge. Make sure you don’t miss out.

Other companies looking to capitalize on the Fourth Industrial Revolution:

BCE Inc. (NYSE:BCE, TSX: BCE) is a Canadian giant. Founded in 1980, the company, formally The Bell Telephone Company of Canada is composed of three primary subsidiaries. Bell Wireless, Bell Wireline and Bell Media, however throughout its push into the position of one of Canada’s top telco groups, it has bought and sold a number of different firms.

BCE is also at the forefront of the Internet of Things movement in Canada. Its Machine to Machine solutions are being used by numerous businesses throughout North America and its new LTE-M network is sure to rapidly increase the adoption of these solutions.

The Descartes Systems Group Inc. (NASDAQGS:DSGX, TSX: DSG) (commonly referred to as Descartes) is a Canadian multinational technology company specializing in logistics software, supply chain management software, and cloud-based services for logistics businesses. The company is making waves in the tech industry with its futuristic products and visionary leadership.

Recently, Descartes announced that it has successfully deployed its advanced capacity matching solution, Descartes MacroPoint Capacity Matching. The solution provides greater visibility and transparency within their network of carriers and brokers. This move could solidify the company as a key player in transportation logistics which is essential in the world of commerce.

Shopify Inc (NYSE:SHOP, TSX:SHOP) is a Canadian e-commerce company. More than 500,000 companies rely on Shopify’s real-time e-commerce, including Tesla, Budweiser and Red Bull, among many others. Shopify makes purchasing goods and services easy for anyone – and in a time where convenience is king, Shopify surely has staying power.

In addition to its revolutionary approach on e-commerce, Shopify is also delving into blockchain technology, making it a promising pick for investors, especially given that the sector is red hot right now.

Celestica Inc. (NYSE:CLS, TSX:CLS) is a manufacturer of electrical devices used in IT, telecommunications, healthcare, defense and aerospace industries. While telecommunications stocks have been volatile recently, defense, IT and aerospace industries have outperformed and while many see limited upside, these industries continue to surprise both investors and analysts.

Absolute Software Corporation (TSX:ABT): This Vancouver-based company offers endpoint security and data risk-management solutions, and though this year has seen a share price dip thanks to the wider market volatility, it is still looking promising.

With strong management, an innovative team, and strong cash flow forecasts, Absolute Software is drawing growing investor attention.

By. Steven Pulver

IMPORTANT NOTICE AND DISCLAIMER

PAID ADVERTISEMENT. This communication is a paid advertisement. Safehaven.com, Leacap Ltd, and their owners, managers, employees, and assigns (collectively “the Publisher”) is often paid by one or more of the profiled companies or a third party to disseminate these types of communications. In this case, the Publisher has been compensated by Frankly, Inc. to raise public awareness of the company and to advertise and market the company’s products and services. Frankly paid the Publisher fifty thousand US dollars to produce and disseminate this and other similar articles and certain banner ads. This compensation should be viewed as a major conflict with our ability to be unbiased.

Readers should beware that third parties insiders and/or their affiliates may liquidate shares of the profiled companies at any time, including at or near the time you receive this communication, which has the potential to hurt share prices. Companies profiled in our articles frequently experience a large increase in volume and share price during the course of public awareness marketing, which often ends as soon as the public awareness marketing ceases. The public awareness marketing may be as brief as one day, after which a large decrease in volume and share price may likely occur. This communication is not, and should not be construed to be, an offer to sell or a solicitation of an offer to buy any security. Neither this communication nor the Publisher purport to provide a complete analysis of any company or its financial position. The Publisher is not, and does not purport to be, a broker-dealer or registered investment adviser. This communication is not, and should not be construed to be, personalized investment advice directed to or appropriate for any particular investor. Any investment should be made only after consulting a professional investment advisor and only after reviewing the financial statements and other pertinent corporate information about the company. Further, readers are advised to read and carefully consider the Risk Factors identified and discussed in the advertised company’s SEC, SEDAR and/or other government filings. Investing in securities, particularly microcap securities, is speculative and carries a high degree of risk. Past performance does not guarantee future results. This communication is based on information generally available to the public and on an interview conducted with the company’s CEO, and does not contain any material, non-public information. The information on which it is based is believed to be reliable. Nevertheless, the Publisher cannot guarantee the accuracy or completeness of the information.

SHARE OWNERSHIP. The owner of Safehaven.com owns shares and/or stock options of the featured companies and therefore has an additional incentive to see the featured companies’ stock perform well. The owner of Safehaven.com has no present intention to sell any of the issuer’s securities in the near future but does not undertake any obligation to notify the market when it decides to buy or sell shares of the issuer in the market. The owner of Safehaven.com will be buying and selling shares of the featured company for its own profit. This is why we stress that you conduct extensive due diligence as well as seek the advice of your financial advisor or a registered broker-dealer before investing in any securities.

FORWARD LOOKING STATEMENTS. This publication contains forward-looking statements, including statements regarding expected continual growth of the featured companies and/or industry. The Publisher notes that statements contained herein that look forward in time, which include everything other than historical information, involve risks and uncertainties that may affect the companies’ actual results of operations. Factors that could cause actual results to differ include, but are not limited to, changing governmental laws and policies concerning, among other things, data protection and data privacy, the size and growth of the market for the companies’ products and services, the companies’ ability to fund its capital requirements in the near term and long term, pricing pressures, etc.

INDEMNIFICATION/RELEASE OF LIABILITY. By reading this communication, you acknowledge that you have read and understand this disclaimer, and further that to the greatest extent permitted under law, you release the Publisher, its affiliates, assigns and successors from any and all liability, damages, and injury from this communication. You further warrant that you are solely responsible for any financial outcome that may come from your investment decisions.

TERMS OF USE. By reading this communication you agree that you have reviewed and fully agree to the Terms of Use found here http://Safehaven.com/terms-and-conditions If you do not agree to the Terms of Use http://Safehaven.com/terms-and-conditions, please contact Safehaven.com to discontinue receiving future communications.

INTELLECTUAL PROPERTY. Safehaven.com is the Publisher’s trademark. All other trademarks used in this communication are the property of their respective trademark holders. The Publisher is not affiliated, connected, or associated with, and is not sponsored, approved, or originated by, the trademark holders unless otherwise stated. No claim is made by the Publisher to any rights in any third-party trademarks.